FruitTrop Magazine n°240

April 2016 -

Avocado &

Banana close-ups

- Publication date : 11/05/2016

- Price : Free

- Detailled summary

- Articles from this magazine

In Africa, they have long been able to brew beer from bananas. In Europe, the 2015 summer season showed that champagne could be produced from avocados! With the supply on the up yet well within the capabilities of European demand, 2016 will not be of the same ilk, but is still set for a respectable performance, at least on paper. A large part of this season’s success will be played out across the pond, on a US market just as avid for the avocado as ever, but where Mexico is increasingly leaving its competitors in the shade, and not only during the winter season. This trend will not be without consequences on the supply to the European counter-season market in the medium term.

The 2016 season initially augured well, with the expected production level set to confirm the surge of the South African cultivation area (approximately +500 ha per year for the past few seasons). However, the weather was particularly bad in late 2015-early 2016. On the one hand, the major avocado zones in the north of the country were hit by severe drought, though the widespread use of irrigation helped mitigate its effects. On the other hand, Limpopo was hit by two hail storms, one of which in February was particularly devastating for the Tzaneen zone, reported by the South African press as “the worst for the past twenty years”. Some plantations, thankfully fairly few in number, were so badly affected that they will need to be uprooted. Hence the overall export potential should not exceed 12.8 million boxes, a figure similar to the 2015 and around average for previous seasons, though disappointing in comparison to the initial forecasts. Certain exporters actually believe that this objective will be difficult to achieve, as the sorting rejects due to superficial damage caused by hail or even to the sizing, which is set to be distinctly smaller than in the 2015 season, are difficult to estimate. Just as in previous years, practically all the volumes will again be aimed at the European market, since although the talks on opening up the US borders are making progress, they have still not borne fruit. The local market, still making strong progress (55 000 to 60 000 t consumed in recent years), will continue to represent a useful alternative.

Just as in 2015, Peruvian production will not make the progress heralded by the boom in surface areas, which have gone from less than 10 000 ha at the beginning of the decade to approximately 25 000 ha in 2016. Temperatures have been abnormally high in the north of the country, limiting the boom in production by major provinces such as La Libertad (an area irrigated by the Chavimochic project) or Lambayeque (an area more recently irrigated by the Olmos project). Hence, though the Hass export potential, at just over 190 000 t, is up considerably from 2015 (approximately + 20 %), this is a level well below those of 2010 to 2014 (more than 30 % on average). If we go by the initial schedule for each market, the bulk of the increase in volumes should be absorbed by the European market (approximately 130 000 t of Hass, i.e. + 15 %). The quantities earmarked for the United States are conservative (approximately 50 000 t, just as in 2015). The diversification markets should absorb increasing volumes, especially thanks to Japan and China, which opened up their borders at the very end of last season, but which will nonetheless remain moderate (less than 10 % of the total potential). The calendar is set to be slightly earlier than in 2015, since the high temperatures which have affected the north of the country have accelerated fruit maturation.

Kenya has constantly increased its presence on the Community market in recent years, with Hass volumes practically doubling in the space of five years, to near the 10 000-t mark in 2014 and 2015. The source has also improved its credibility thanks to the efforts made by the industry as a whole to raise the quality level of the supply. This rise to prominence should continue in 2016, with exports to the EU expected to be up slightly. On the one hand, as far as we can judge, the harvest level seems to be fairly good, as the rainfall has been rather decent. On the other hand, there are new exporters in the arena, and the cost of freight, down considerably from last season, provides a substantial incentive.

So what about the outsiders? Tanzanian exports should be similar to their 2015 level, i.e. approximately 3 500 t, aimed entirely at the EU-28. There has been considerable growth in surface areas in recent seasons, which is continuing at a rate of around 100 to 160 ha, in both the north and south of the country. However, one of the two zones is set for a negative alternate bearing effect. The rainfall has been below normal, though without causing drought. So the sizing should be fairly good, especially since the orchards are young.

Conversely, the Brazilian presence should be a bit bigger. After a negative alternate bearing effect in 2015, with unfavourable weather, Hass production, primarily packed into the Sao Paulo region, should be back to a higher level in 2016. Hence exports to the EU-28 should be around 4 000 to 5 000 t.

If these predictions come true, the overall supply should rise by approximately 10 % from last season; a figure below the 20% growth in European demand between 2013 and 2014, and 13 % growth between 2014 and 2015 (see inset). True, the consumption dynamic has not been so positive if we focus the analysis on the summer 2015 season alone (volume increase “only” 6 %), but that was clearly for lack of merchandise. The barely imaginable rise in the campaign average price (50 % from 2015, exceeding 10 euros/box for the first time) clearly demonstrates that the market could have consumed much greater volumes than were available.

Will the market be able to start the new season on the right foot? The high prices seen in April for the past several years are of course positive for the industry, but they also have the adverse effect of encouraging certain exporters to start their campaigns too early, with immature merchandise. This leads to several serious consequences. On the one hand, selling such fruit, especially at high prices, tends to curb consumption, which really needs a boost before the sharp peak in incoming shipments in mid-May. On the other hand, it is not only the brand image of the exporter which is tarnished, but also that of the source. We cannot help but observe that the 2016 season is not off to a very good start at the time of writing, despite the widespread implementation of protocols stipulating a minimum dry matter content for export. Inspection efforts need to be stricter, especially in Kenya and Peru.

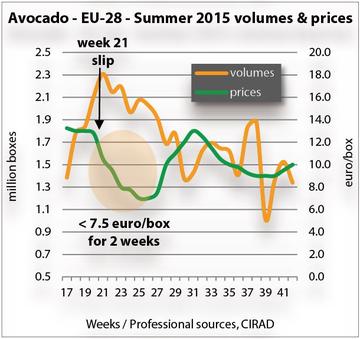

Just as in previous years, the distribution of volumes over time will be crucial for the success of this campaign. Last season showed how risky a period June is, when the South African and Peruvian incoming shipment peaks start to overlap: prices plummeted in week 23, after three successive weeks of an overall supply of between 2.1 and 2.3 million boxes. However, this dangerous corner was negotiated safely, thanks to a quick return to more moderate incoming shipments. It is worth reiterating that this was not the case in 2014, with the market tipping towards a protracted major crisis (13 weeks of prices between 5.50 and 6.50 euros per box!). Once again this season, we will need to avoid falling into this recurrent trap.

To do so, we will need to rely more on correct adjustment of the supply than on how demand can perform. We should emphasise that it was sound management of volumes which kept the slip under control in 2015, since the actions implemented by the supermarket sector to stimulate demand proved limited at best. It is hard to raise interest from the supermarkets in the avocado at this time of year, despite the importers’ efforts, while the seasonal fruits and vegetables supply is on the up. In France, the only country for which we have numerical indicators, the action was limited to one week of promotions, while prices came undone for one month. In addition, the scope of these promotions was modest (promotion rate of 13 %, as opposed to a peak of up to 20 to 25 %, including at this time of year), while retail prices actually returned to a comfortable level of 1.10 to 1.16 euros per fruit (i.e. a no less comfortable margin of more than 12 euros/box), after a mere week of significant reductions. The promotions do not seem to have been any more numerous or effective on the other European markets. The early June corner appears no less hazardous this season. True, the market’s equilibrium point is probably ten percent higher than last season, given the consumption growth reservoirs, but this should not be exceeded. So there is only one solution: stagger the volumes as much as possible. We should emphasise that this is a win-win strategy, since it not only helps prevent prices from plummeting to depths from which they will not be able to recover for a long time, but can also capitalise on a more limited supply, with the promise of decent rates in August.

While, as we have seen, there are risks for this 2016 summer campaign, the expected rise in volumes appears to be within the growth capacities of European demand. Yet one key point remains to be confirmed: the ability of the United States to absorb the programme planned by Peru. This market seems much less open than in 2015. True, there should be no lack of demand, with continued progress expected. The 2015 figures show a very strong recovery in the growth dynamic, which contrasts with the distinct slowdown in 2014: the volumes absorbed were up by 19 % from the previous season, without any major price reduction (down 7 %). Even the west of the country, an over-consumption zone which seemed to be starting to run out of steam for the past two years, has bounced back (up by around 15 % in California and in the rest of the West). Nonetheless, it is set for a particularly abundant supply, with volumes up considerably from the two major suppliers.

After two lean seasons in 2014 and 2015, Californian production is back to an “average” level in 2016. The 180 000 t expected is nothing exceptional (between 230 000 and 240 000 t harvested in 2012-13 and 2009-10), yet this level nonetheless represents a rise of 40 000 to 50 000 t from the previous two seasons. This recovery is due mainly to the more abundant rainfall in this El Niño year, which has helped forestall — at least temporarily — a drought which has persisted since the beginning of the decade. However the sizing appears on the average to small side.

Another cause for concern for Peru is that the competition from Mexico could well be much stiffer than in 2015. The more than 30 % increase in shipments from Michoacán to the United States since the beginning of the 2015-16 season (July to March) provides a clear hint. This bald percentage conceals a figure of 200 000 t of additional exports, thanks to a record harvest estimated at 1.5 million tonnes and to ever greater surface areas approved for export every year! The US market specialists believe that the “king of the avocado” State should maintain its massive flow until the big “Cinco de Mayo” promotions, with volumes on the wane thereafter, though still greater than in previous years. Hence Mexico, a supplier enjoying comparative advantages in terms of competitiveness by virtue of its proximity, could well put its competitors in the shade more than usual. Chilean exporters fell foul of this experience during the 2015-16 winter season: shipments to the United States, often in excess of 100 000 t between 2005 and 2010, should barely reach 10 000 t.

The Mexican competition could well end up multiplying this campaign, or at least in the fairly short term. The US market is on the point of opening up to Hass avocados from Jalisco. The authorisation, said to be imminent at the beginning of the year, has seemingly been held up somewhat, though it could still come this summer if we believe the US market specialists; and this is an issue that matters. True, this State’s production is not on the same scale as its neighbour Michoacán. Nonetheless, it is among the top five in the world, with an average of approximately 150 000 t. Secondly, the harvest, which is based in large part on the early cultivar Mendez, and peaks from June to August, is the perfect foil for Michoacán, which has its low point at this time of year. With the forthcoming accreditation of this source, the Mexican Hass will become available in large quantities year round, and especially during the Peruvian Hass marketing period. Some big names in the US avocado market such as Calavo have already invested in this State, building a packing station in Ciudad Guzman.

The issue of the outlet for fruits from the young Peruvian plantations, which have recently entered production or about to do so, will become increasingly pointed in the coming years. On the one hand, because the volumes in play are particularly big: with a high-yield Hass cultivation area of 24 000 ha, the prediction by the CEO of Prohass for the Peruvian export potential to double before the end of the decade should come true (400 000 t). On the other hand, because the US market appears to be structurally less and less open. True, US consumption, driven by the mighty promotion machine that is the HAB, has again demonstrated its power. And maintaining a growth rate of 10 % per year (i.e. a trifling additional 100 000 t or so per year) is perhaps not a pipe dream, in particular if the Mexican peso/USD exchange context, particularly promising this season, holds up. It is also true that Californian production should at best hold up, with surface areas shrinking and a structurally critical problem of agricultural water availability and cost, barring this atypical El Niño year. Nonetheless Mexico, or rather “the Mexicos”, which enjoy a level of competitiveness difficult to equal due to their proximity to the United States, seem to be very much in a position to supply the vast majority of the volumes required. According to the USDA, the surface areas increased by more than 25 000 ha between 2010 and 2015 in Michoacán, where yields range from 8 to 16 t/hectare. Furthermore, Jalisco’s entry will probably have a major impact. It is in direct competition with Peru, since the cultivation stock mainly comprises Mendez, and volumes are set to progress steeply, with just over 17 000 ha in cultivation, of which more than 8 000 planted between 2010 and 2015, with an average productivity of around 15 t/ha. Furthermore, while available surface areas are starting to become scarce in Michoacán, Jalisco retains plenty of potential, as well as a much calmer political climate favourable for investment.

So a large part of the additional production expected in Peru in the coming years should instead be earmarked for the world’s other great consumption centre, namely Europe, and for the diversification markets. They need to ensure that the enormous growth margins for consumption still available in Europe and the rest of the world develop in line with the rapid surge during the supply summer season, especially from Peru. The creation, at the Lima Conference, of a promotion tool designed along the lines of the highly effective HAB, with a worldwide scope, is undeniably very good news in this context

Click "Continue" to continue shopping or "See your basket" to complete the order.

{kind=link}