Recovery confirmed

2015 confirmed the renewal of Southern Hemisphere production, after two years of steep falls due to Psa (

Pseudomonas syringae pv.

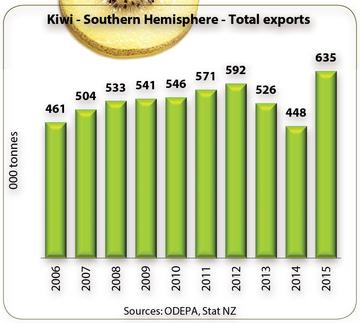

Actinidiae) and to the frosts of 2013 in Chile. Production actually appears to have set a record level of nearly 650 000 t (+ 46 % on 2014), well above the 618 000 t harvested in 2010. Exports also leapt up by 43 %, setting a new best of 639 000 t. There was a considerable increase to the European market (+ 33 %), though without regaining the nearly 300 000 t back in 2008 (200 000 t for New Zealand and 100 000 t for Chile). It was even more marked on the US market (+ 53 %), where tonnages were as high as in 2012. Similarly, shipments aimed at Russia were 45 % higher, where New Zealand has been down for the past two years because of Chile making its comeback and maintaining its market share on this outlet. Shipments also continued to rise steadily to Asia (+ 39 %), with New Zealand branching out to these nearby destinations and Chile returning to levels close to their pre-frost mark. The latter source also won back market share in Latin America and the Middle East, though tonnages were still a bit lower than in previous years.

kiwi - southern hemisphere - total exports

kiwi - southern hemisphere - total exports

Confidence riding high in New Zealand

New Zealand confirmed the rude health of its industry, boosted by new varieties, especially the Zespri SunGold. Thus, after reaching its low point in 2013 (361 000 t), New Zealand production literally boomed last campaign (475 000 t, i.e. + 30 % on 2014) to exceed the pre-Psa level (435 000 t in 2010). The bacterium is still abundant in New Zealand’s orchards, but all the new varieties are now resistant, including the green kiwis. Producers have learned to live with this threat. The control methods are well managed and applied by producers to prevent propagation. They are particularly vigilant in identifying the now well-known symptoms of the disease and immediately cutting out infected sections. Copper sprays are authorised at low concentrations on pruned trees, and preferably before rain, as the operation must never be carried out in wet conditions.

The production increase primarily involves the yellow kiwi. The good results from the past two campaigns have restored producer confidence. There was massive planting last season, which, in addition to the grafting of Hort 16, raised the total to 4 800 ha of yellow kiwi, i.e. 36 % of the total kiwi cultivation area. This should continue at a decent rate over the coming years, since Zespri has taken the decision, given the very strong demand, to authorise the planting of an additional 400 ha from this year until 2019. The green potential is also back on the up, with increased yields having taken the export level back over 300 000 t in 2015, whereas yellow kiwi exports exceeded 100 000 t. The eventual objective is to reach a 50/50 balance between green and yellow kiwis, which could be reached after 2020. Hence New Zealand production at present covers more than 12 000 ha already in production, and a planted area of more than 13 000 ha, i.e. a potential which should further increase to rapidly reach more than 570 000 t from 2018. The industry is also continuing its varietal trials. Approximately 100 000 different plants are currently being assessed. Zespri has a new red-fleshed variety at the pre-commercial trial stage.

Efforts which will ultimately bear fruit in Chile

Chilean production has not yet stabilised. After steadily increasing until 2012 (11 900 ha), surface areas have been decreasing for the past three years (9 700 ha in 2015), between uprooting due to Psa and economic difficulties. However, production returned to around 180 000 t during the last campaign, after the frosts of late 2013 which had more than halved the potential. However, it did not regain its previous level due to the after-effects of the frosts and Psa (220 000 t in 2012). Today, Psa affects at least 20 % of Chilean territory, which is 15 % green varieties and 40 % yellow varieties, which are more sensitive, especially the Kiss variety. However, yellow kiwis make up no more than 800 ha, half of which is Jintao (Jin Gold). Hence the choice of the production zones is crucial for producers who want to develop this niche: the north of the country and the coastal zones are advisable, insofar as climate conditions are less favourable there for Psa. Preventive measures have been implemented to prevent its propagation, but the inspections are demonstrating that they are still insufficiently applied for the time being. Besides the measures taken in the field (foot baths, monitoring, pruning and tool cleaning), producers are advised in particular to be vigilant when shipping the fruits to exclude any plant debris and cover the loads. Similarly, strict disinfection protocols have been established at stations for washing the trays, as well as for the destruction of plant waste from packing. Furthermore, the Chilean Kiwi Committee, which monitors the application of these measures, has this year also worked on raising the overall quality level of production, establishing a minimum value of 14.5 % dry matter in the harvest, to tackle New Zealand competition on the export markets.

kiwi - southern hemisphere 2015 exports

kiwi - southern hemisphere 2015 exports

Good volumes expected this campaign

The stabilisation of the cultivation area after the Psa outbreak is heralding a rise in potential over the coming years. This year, it should be similar to the good level already harvested last year. The Chilean potential is set to be 10 % in shortfall (165 000 t, as opposed to 183 000 t in 2015), because of an autumn lacking in hours of cold, which affected the flowering, and a wet spring followed by a warm summer. New Zealand production meanwhile should again approach or even exceed 480 000 t.

Hence the quantities exported should be at least fairly similar to last year. Zespri has announced an export potential at least equivalent to the previous one, with green volumes perhaps a little smaller, of between 280 000 and 300 000 t, though distinctly greater for yellow. Notably for this campaign, the first ship from New Zealand, which docked in Zeebrugge in late April, contained only yellow kiwis, with the first green kiwis arriving only in mid-May. However, the source is thinking about ending the Sungold campaign in around mid-September. Conversely, things are set to be particularly complex for Chile, whose campaign began in mid-March. Penetrating the European market is becoming increasingly difficult for this source, in the face of the increasingly late local produce and the increased competition from New Zealand not only on the Old Continent, but also in Asia. However, operators are hoping to be able to capitalise on the qualitative level of production, with sizing bigger than last year and a higher dry matter content, in order to meet the new maturity criteria set by the Chilean Kiwi Committee

{kind=link}