"Desperate case” or “textbook case” - there is no lack of characterisations for the European sea-freight pineapple market. The first option definitely has a little too much finality. The pineapple market will always be a market where volume prevails over quality – this battle is long lost. Advocates of this option, definitely the grouchy sort, observe that the sole value level regulator for imports, and therefore production, is the supply level. Non-price competitiveness has little place in a market operating like this. The weather or producer bankruptcies set the supply level, to which the prices adjust. In a way, it is a perfectly “neoliberal-compatible” market. The supply/demand curve adjusts to the price.

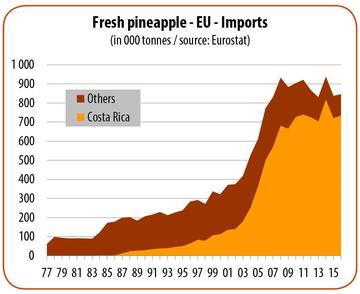

The European figures confirm this hypothesis. In 2014 this market reached breaking point. At the time, the EU imported nearly 940 000 t of pineapples, i.e. a leap of 300 000 t in just a decade. So on the face of it, everything was going well. On the flip side, it was an economic catastrophe! The import price dropped below 7 euros per box, i.e. the lowest point ever reached (by annual average). Serial bankruptcy in Costa Rica, due to piteous economic returns, triggered a fall in supply which from the first months of 2015 resulted in a highly dynamic bounceback in import prices. The 2015 average gained 2 euros per box to reach 9 euros, a level which was fully confirmed in 2016. Consequently, the equilibrium point between a depressed market and a value-creating market appears to be situated below 850 000 tonnes. True, this analysis is limited to comparing annual price and volume results. Things get more complex if we look at this market weekly or monthly. The volatility varies, but in every case depends on the market supply tempo by Costa Rica. This was again the case over the first four months of 2017.

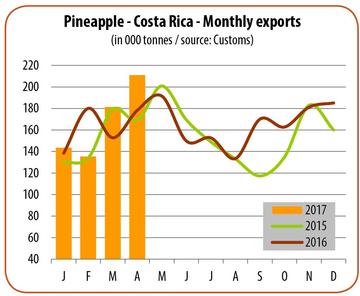

During Q1 2017, Costa Rica cut sail by approximately 10 000 t, compared to the same period in 2016, enough for prices to maintain levels comparable to those of the same period of 2015 or 2016. Unfortunately, this was not down to better management of volumes upstream, but rather the undesirable and uncontrollable effects of bad weather in 2016, due to the dreaded El Niño phenomenon. The upshot was alternating droughts and intense rains at the end of the year, which prevented natural flowering and therefore led to a reduction in shipments from Q1.

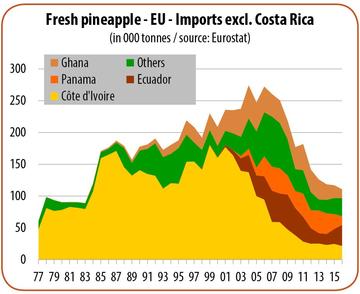

fresh pineapple - EU - imports excl costa rica

fresh pineapple - EU - imports excl costa rica

fresh pineapple - EU - imports

fresh pineapple - EU - imports

The supply took an upturn in April, though without weighing down on prices, due to a positive demand trend throughout Europe: an auspicious period in terms of demand for tropical fruits (Easter promotions), under-supply in March, very low pressure from competing fruits, cold temperatures, etc. From May, the supply was bigger with prices on a downward trend - QED. Volume and price are invariably in unison for the better, but more often for the worse. Yet invariably need not necessarily mean inexorably.

There is nothing inevitable in this market becoming a mere agricultural commodity. It has a completely different potential. The pineapple enjoys a host of intrinsic values: it is widely known to the public, but retains a highly exotic character, it has an original set of assets (colour, eyes, crown), its renowned nutritional qualities, etc. So why make it a basic product, even to the point of removing its crown? The destiny of the pineapple is not to be reduced to the plebeian ranks of the potato or banana. On this point I would like to hesitate with the characterisation proposed at the beginning of the article: “textbook case”. The same textbook tells us that on a mass market, the supply must be segmented to get ahead. That is what certain operators are doing. The pineapple volumes concerned are still limited, though they are generating enthusiasm since this is the only way out of the poor house for the pineapple.

One of the pineapple’s lifelines lies between the fresh and processed sectors. Indeed the ready-to-eat processed pineapple, which has a rather short shelf life (pre-prepared fresh products, fresh-cut, etc.) is gaining space on the shelves. Things are developing rapidly, and many operators are getting into this niche with differentiated strategies: from processing factories on the import markets to cutting fresh fruits in-store. This is along the same lines as orange juice machines, located in transit points but also in the fruits & vegetables section itself. Yet creation of additional added value primarily, or even exclusively, concerns the downstream segment of the industry. Fresh fruit is imported for processing. The quality criteria for this kind of fruit are different to, and on certain points, more permissive than the fresh segment. So this is doubtless very good for consumption in general, though not really revolutionary for the upstream part of the industries.

Another lifeline, this time more conventional, is also being explored or rather rediscovered. What do marketing law texts tell us? Segment to improve your gain. And to segment, you first need to ensure the quality and therefore reassure customers. One way of doing so - for sure not the only way - is to control its supply, i.e. the agricultural and logistical practices upstream of importing. Quality, the watchword par excellence often a little too handy to be honest, can also be a vehicle of real added value, with no green, social or quality washing. Compliance with a degrees brix, a brix/acidity ratio, a coloration (internal more than external), the absence of physiological faults or storage diseases, commitments to good agricultural practices respecting people and their environment, local speciality, etc. Lots of things can be done, and are currently being tried. In the same vein, the customer need to be retaught (consumers and supermarket sector purchasers) that the external coloration of a fruit does not truly indicate its intrinsic quality. So there is a long road, since every time you need to deconstruct the myths of the beliefs anchored for more than twenty years in the customs of the sector and consumers. The distribution sector must also be receptive to these efforts, and support the operators which want to do things differently.

pineapple - costa rica - monthly exports

pineapple - costa rica - monthly exports

sea freight sweet pineapple - germany - import price

sea freight sweet pineapple - germany - import price

{kind=link}