FruitTrop Magazine n°247

March 2017 edition: Mango close-up. The latest on the date market, berries and sea freight.

- Publication date : 4/04/2017

- Price : Free

- Detailled summary

- Articles from this magazine

One of the major differences between the container shipping and reefer shipping industry dynamics is the role played by the reefer lessors. In the economics of reefer container shipping the lessors play a pivotal role. In many ways the lessors have become the financiers of the containerized cold chain

At the start of 2017 the specialized reefer fleet stood at 539 reefer vessels with a total below-deck capacity of 183m cbft. If freezer vessels are included, the numbers swell to 625 vessels and 204m cbft respectively. The average age of the fleet is 27 years. At an average of 20 years, the youngest segment is the largest units (600 cbft), while at an average of 32 years, the oldest segment is made up of vessels in the 100-199 cbft range.

The start of 2017 has already seen a number of vessels either change hands, switch pools or set sail for demolition on the beaches of the Indian subcontinent. Seatrade has been either directly or indirectly responsible for the majority of the changes to date: the operator has had to divest tonnage in order to find a home for the units redelivered at the end of 2016 from Fyffes/Turbana, De Nadai and Del Monte at a time when its new Colour Class vessels are added to its fleet.

If the charter market activity remains weak and yields show no sign of strengthening from last year, the first half of 2017 is likely to see a steep year-on-year rise in the number of vessels demolished. With higher bunker prices offsetting the limited gains made on rates, a disappointing squid season on the cards and large units interfering in the core small segment trades, a significant cull of less efficient tonnage is surely inevitable.

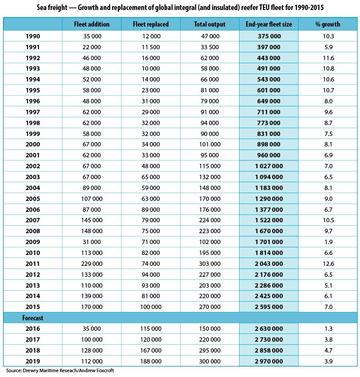

Meanwhile, the scale and duration of the downturn in the container business is reflected in the figures and forecast for reefer container manufacture in 2016 and 2017. According to the latest Drewry Maritime Consultancy statistics, the global reefer container fleet will increase by 1.3% in 2016 to 2.63m TEU (1.32m FEU). The percentage increase is the lowest on record – lower even than the figure for 2009, the height of the global recession.

In absolute terms the fleet increased by 35 000 TEU (17.5K FEU) by the end of the year as the highest ever number containers (115K TEU) were scheduled for decommissioning, according to Drewry. The total number of reefer boxes manufactured is forecast at 150K TEU, the lowest since 2009. To put these figures in perspective, with the addition of the now fully operational MCI container plant in San Antonio, the total global manufacturing capacity of reefer containers stands at approximately double this figure.

One of the major differences between the container shipping and reefer shipping industry dynamics is the role played by the reefer lessors. Simplistically, the reefer ship is a fixed cost, floating fridge. The fixed cost container vessel functions only with variable cost equipment. Reefer capacity is limited by the number of slots on the vessel but determined by the number of reefer containers utilized. The containers are either owned by the carrier or leased from specialized lessors.

Now, the reefer lessors currently hold an approximate 40% share of all reefer containers in the market: less than a decade ago, this share was roughly 30%, but since the economic crisis in 2008-09 the lessors have taken a significantly more prominent role. Indeed over the past five years, the ratio of reefer containers manufactured stands at 70:30, lessors:carriers!

In the economics of reefer container shipping the lessors play a pivotal role. In many ways the lessors have become the financiers of the containerized cold chain as the crisis affecting the container shipping industry has worsened. They provide vital support to the reefer ambitions of the carriers - without the equipment made available to the carriers by the lessors, the lines would not have been able to grow their share of the reefer trades.

Indeed, were the lessors not to exist, the annual global investment in the manufacture of reefer containers (at USD15 500-16 500 per unit) would undoubtedly be significantly lower. This is because under current economic conditions, most carriers cannot afford to invest in replacing, let alone building their own reefer container capacity – for example, of the 30% share of total manufactured units attributed to the carriers over the past 5 years, in 2016 it was only Maersk Line, CMA-CGM, Matson and Hapag Lloyd that made any materially significant investment.

More trouble lies ahead – in the short term, the carriers will become even more dependent on the lessors. Ever larger container ships are being delivered onto a market that is heavily over-saturated. The conundrum is as follows: without the reefer containers, there is no contribution to revenue on the service strings in which reefer is involved. And, the bigger the ship, the higher the number of reefer plugs and the greater the potential therefore for lucrative reefer revenue! Under current circumstances, the lessors have the carriers on toast – so one would naturally expect that the per diem rate ‘currency’ would reflect the imbalance in power?

Well…. actually, no! From 2014 until late 2016 lease rates remained seriously depressed, as here too there has been oversupply. The combination of the low cost of finance, low cost of manufacture and the high degree of industry fragmentation on the one hand and weak demand on the other, led to per diem rates falling to little more than USD4 for delivery in the Americas and just under USD4 from the Chinese factories. Although these rates have recovered from those historical lows to USD5-plus at the start of 2017, this level is still unsustainable for investment returns in the short term, let alone the medium to long-term of the equipment lifecycle (12-15 years).

To date, the lessors have failed to leverage their substantial equity. If they want rates to rise, it is patently not in their interests to commission more new reefer containers. And there are signs this may be about to change. Firstly the cost of equipment is rising, while the era of cheap finance is coming to an end – every 1% rise in the base interest rate adds approximately USD0.50c in cost to the per diem lease rate. The lessors took heavy collateral damage following the collapse of Hanjin in August last year; the knock-on impact is that two lessors have temporarily been obliged to suspend any newbuild activity. Finally, the industry has consolidated to four major players, a reflection of the ongoing difficulties faced.

Drewry estimates total manufacturing output in 2017 at 220 000 TEU (110 000 FFE) a near 50% increase year-on-year and valued at USD1.75bn approximately. On current and likely short-term metrics, this figure makes no sense. Even less so given the operational synergies anticipated when Maersk Line absorbs Hamburg Süd later this year, along with other potential boxline industry mergers.

Click "Continue" to continue shopping or "See your basket" to complete the order.

{kind=link}