FruitTrop Magazine n°215

Pineapple close-up

- Publication date : 29/10/2013

- Price : Free

- Articles from this magazine

The Victoria pineapple 2012-13 season was relatively quiet. It is still considered a primarily festive fruit by operators and purchasers, hence it sold best during the end-of-year holidays. It is a relatively limited market, which struggles to reach 3 000 tonnes.

During last season, demand for Victoria did not see any real periods of frenzy. It remained in line with the supply, maintaining some degree of fluidity in its sales and rates. However, several operators lamented the delays or difficulties encountered in promoting Victoria for the festive periods. These problems were reportedly due to demand, which since the 2008 crisis, has seemed to indicate consumers waiting for the last minute to make their holiday purchases.

Hence the supply, which did not see any periods of very large-scale procurement or shortfall, contributed to maintaining some degree of price stability throughout the season.

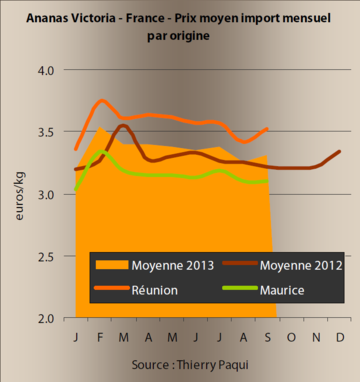

Mauritius and Reunion were the main sources which supplied the markets. The prices paid at the import stage for these two sources remained good, though last season confirmed that the Reunion supply had some degree of superiority. Although smaller in volume, it is often rated to be better quality than the Mauritius supply, with its relatively small volume also enabling it to get better value on the market.

The wholesale markets and specialised traders remained the main outlets of the Victoria. Demand continued to favour sizes 6, 7 and 8, which were less available and more valuable. Over the whole season, average rates at the import stage fluctuated between 2.85 and 3.50 euros/kg for Mauritian fruits, and between 3.30 and 3.85 euros/kg for Reunion fruits.

Weeks 40 to 48 marked the beginning of the season. Although this period coincides with the end of the stone fruit season, demand was still late in switching to small exotic fruits. The supply, which had hitherto been limited, was increasingly substantial, especially from Reunion. Sizes 6 and 7 were in short supply, and were particularly sought after. Nonetheless, despite the relative weakness of sales, rates remained stable.

In December, demand was still slow in getting going. The operators were showing some concern, since they were struggling to clear all of their stock from one week to the next, while rates remained stable. Sales were proceeding as per usual, with no real desire to promote the fruit for the end-of-year holidays. The operators feared that the volumes expected in anticipation of the festivities could end up being sold off at low prices to avoid market saturation. Fortunately this was not the case. Indeed, after the first half of December, there was a revival in the market and demand, previously lifeless, picked up again. Rates rose to peak in the last week of the year.

From the beginning of the year, demand and supply subsided. As is often the case after the holidays, the operators abandoned the Victoria. Nonetheless, the rates did not drop, and remained stable since the supply was in line with the weak demand.

The winter holidays period, which generally brings about a slight downturn in demand, was marked by a fall in supply which continued from week 6 to week 12, with some operators even struggling to re-stock. Nonetheless, demand was not very high, and just barely managed to absorb all of the small volumes on the market week after week.

The Easter sales were not very dynamic. The operators noted the lack of interest in the fruit from purchasers. However, prices maintained a fairly good level during weeks 13 and 14.

During the period that followed Easter, prices were very high and demand fell considerably. We can also point to the quality concerns (internal brown stains) which affected Reunion fruits, forcing operators to reduce their supply pending better-quality shipments. This reduction in imports, which could no longer manage to satisfy demand, partly explains the high prices charged in April. It was Victoria pineapples from Reunion, more sought after but less available, which made the best of the situation to obtain the best market prices.

The fall in the supply continued in May. Indeed, in anticipation of the start of the summer fruits season, operators began to further cut their imports. However, because of the lifeless demand, they had difficulties clearing their stocks from one week to the next. Despite the lifelessness of demand, rates did not fall, due to the overall supply shortage.

The lateness of the seasonal fruits had no effect on demand, which remained fairly low throughout the summer. During weeks 23 to 35, the Victoria supply kept shrinking. Several specialist Reunion operators began their melon season from the same source. In July, despite the weakness of demand, prices were very strong, above all for Reunion produce, though these sales involved only a limited number of fruits.

At the end of the season (weeks 36 to 39), despite the operators returning from their break, demand remained limited without the prices being affected. Indeed, they even saw a slight rise at the very end of the season, more due to the shortage of the overall supply than to demand being in good shape .

Click "Continue" to continue shopping or "See your basket" to complete the order.