FruitTrop Magazine n°228

Pineapple close-up

- Publication date : 20/12/2014

- Price : Free

- Articles from this magazine

While pineapple volumes sold took an upturn in 2014, on the price side nothing seemed to changeon this market, which is on the brink of crisis, without ever completely slipping in. Costa Rica verged on 2 million tonnes of exports, out of the estimated worldwide trade of 2.8 million tonnes. It has a total hold over the European market (estimated at 1 million tonnes) and the US market (1.1 million tonnes), where its market share is between 85 and 90 %.

Lacking innovation or a generalised quality policy, and sagging under the volumes, the sector remains mired in mediocrity.

After several years of lean calves, the world fresh pineapple market seems to be taking an upturn, at least on the volumes side. Indeed both the United States and the European Union have beaten or equalled their historic levels. The United States exceeded for the first the one million-tonne mark, with 1 073 000 tonnes. The EU verged on 930 000 tonnes of imports, a level already reached in 2008. These figures will need to be revised over the coming months. In fact, the Customs services will publish their initial estimates for the whole year in February or March 2015. However, it is a reasonable bet that they are in the right ball park. Since while on the production side the pineapple lends itself perfectly to industrial management, i.e. scheduling (triggered flowering, management of sprout populations, and therefore of replanting years in advance, homogenisation of harvesting stages, etc.), it is also running like clockwork on the trade side… at least in terms of volumes on the market.

As absolute proof: if we take the imports onto the two main markets mentioned (United States and EU) over the first nine months of the year rounded to an annual figure, and if we repeat the exercise over the last six years, the result is indisputable. Imports over the first nine months of the year represent between 73 and 76 % of the annual total. The average is 75 %, with a standard deviation of just 1.4 %. So the future is easy to predict, at least in terms of volumes on the market.

There is no such euphoria — to put it mildly — on the value side. We are a long way from the times when the pineapple was the stuff of investors´ dreams. Just a few years ago, there was no need to hesitate in referring to a big national deal in certain Central American countries. It is now hard to find a source that dares to claim any growth on this product. There is a long list of suppliers abandoning this market, or at least scaling back.

Ecuador, the banana giant, chanced its arm in the early 2000s. Since 2007, it has reduced its presence in the United States, now with exports representing just one tenth of what they used to be. Panama made up its mind later, in the late 2000s, to take the same path, but also abandoned ship very quickly. In 2014 it has exported just one quarter of what it did at its zenith four years ago. For the US market, we will finish off with Guatemala, which it is true has stabilised its export volumes to approximately 15 000 tonnes, but has nonetheless halved them in less than a decade. Among the qualified successes, we can mention Mexico, which for the past six years has exported 30 000 to 55 000 tonnes, and Honduras which is seeing steady growth, reaching practically 40 000 tonnes in 2013 and 2014.

The situation in Europe is even more entrenched, with infinitely more sources which have deserted or are deserting the market, such as Ecuador, Honduras or Cameroon, than sources which are growing, such as Benin. Let´s put Côte d’Ivoire, Ghana and Panama in the resilient category, with just a dash of optimism. Since the African continent, which is trying to assert itself on several highly targeted market segments, such as smooth Cayenne pineapple, Sugarloaf and more generally the air-freight pineapple market, now accounts for just 6 % of the supply to the EU, i.e. just under 60 000 t.

So who is ensuring the rest of the consumption, or rather the bulk of it? The supplier which has not yet been mentioned, and which is crushing the world fresh pineapple market under its full weight is of course Costa Rica. Mentioning this supplier only after two pages is a real editorial feat, so tight is its hold on the market. We will just briefly review the success story of the Costa Rican pineapple, which was long due to the company Del Monte and varietal innovation. It is not every day that a new market standard asserts itself, let alone via a new variety (MD-2 or Extra Sweet, its marketing nickname), within a few years stealing the mojo of the dominant source and variety of the time, i.e. Côte d’Ivoire and smooth Cayenne. Enjoying an impeccable logistics service, exemplary agro-technical expertise and a commercial organisation that still leaves nothing to improvisation, the trio Costa Rica/Del Monte/MD-2 has boosted demand. On the two biggest markets (United States and EU), it saw a fivefold increase between 1996 and 2014! Costa Rica exported 1.9 million tonnes in 2013, and in 2014 is set for well in excess of 2 million. Its market share is impressive, verging on a Soviet election result: 90 % for the United States and 85 % for the EU-27. Yet Costa Rica is not limiting itself to these economic areas, since in 2013 it exported its pineapples to more than fifty countries, nor to the fresh pineapple, since it is increasingly exporting pineapple juice.

The dissemination of the MD-2 variety is a case study which is now taught in innovation management classes. Besides a few industrial products, where the rate of innovation is unrestrained, reinvention at regular intervals is a difficult job in the agricultural industry. Since while the electronics sectors, and in particular telephony, schedule the obsolescence of their devices, and call the slightest change in colour or shape a “major innovation”, agricultural production remains constrained by what crop scientists call the pedo-climatic complex, as well as by the varietal potential of the cultivars available. While Apple has released six versions of its Iphone in less than seven years, the MD-2 2.0 remains to be found. And furthermore, what innovations are we talking about? Colour, shape, texture, sugar-acidity balance, disease tolerance or resistance, productivity, etc.? True, there is much to do, but much has already been done with this pineapple variety, and improvements are protracted and costly to obtain, whether via varietal creation (with or without using GMO) or adapting the technical procedures. We are far removed from the ease with which manufacturers can change the colour of the product simply by adjusting a formula or modifying a process. We are in the living world, and this imposes its own tempo on the industry’s desires to develop. There have been a few announcements emerging here and there about a new variety of pineapple, but hopes have just as quickly been deflated.

However, we can mention a major innovation within the grasp of the industry: a real innovation that could change the status of this fruit in the eyes of European consumers. An innovation which would take the pineapple out of the “also-ran” segment and recrown it as the king of fruits. An innovation which does not require any test tube, any transgenesis, any investment in production, or any additional pesticides. It involves simply paying a modicum of attention to the fruits on the shelf. Because you need to be a die-hard optimist to buy — note that we did not say consume — a pineapple under the conditions which some section managers abandon it. But this is a generalised problem. The fruits and vegetables section is short of “grooms”, and it is a long and exhausting crusade to restore the workforce. However, it is only at this price (or rather cost, the distributors argue) that fresh fruit and vegetable consumption, especially for pineapple, will grow. And this is not us talking, it is the distribution sector bosses themselves. In an LSA article in February 2011, the representative of the Federation of commerce and distribution companies (a professional association bringing together the big French chains) noted that “(…) if the section receives particular care, the results very quickly take care of themselves.” And a manager at Casino added: “In terms of differentiating image and turnover weight, the fruits and vegetables section is where it is all to play for.” Perfect! The diagnostic has been established and all the players are agreed. The stakes are crucial, and go beyond just the fruits and vegetables section. So why is nothing moving? No doubt a stupid question, but to which we have never found an answer, besides the fact that it is expensive. True! But it brings in much more than this, including in terms of number of tubes of toothpaste sold.

True, the French Price and Margins Observatory has shown that the chains are already pulling out all the stops in terms of workforce in the sections. Indeed, the costs of dedicated section personnel, states the study published in 2013 (page 314 et seq.), are relatively high compared to the turnover (T/O) and gross margin. The average net margin of the fruit and vegetables section (6 %) as a proportion of T/O is among the lowest of the sections with a positive net margin, in spite of the weight of the section in the T/O (18 %) and gross margin (17 %). So if we believe the figures, we are at a deadlock.

But let’s get back to the pineapple. There is another innovation which is changing, or even revolutionising, the service provided: the processed products very regularly available in stores. These are either “artisanal”, with the pineapple cut before the eyes of customers, against a potent backdrop of tropical music, Madras fabrics and local colour; or industrial, with the pineapple in this case offered in sachets, boxes, pots, etc. This is aimed at the snacking segment, though not exclusively. It is also targeting the higher socio-professional groups. Indeed, for the “industrial” supply, we regularly reach a figure of 20 euros per kilo of fresh pineapple, and even in excess of 30 euros! At this astronomical price, it comes without its skin and crown, as well as the chore of peeling. Better still.

But are we actually still on the same market? These two segments have plenty in common. The unit of location is practically a common factor. In the case of the processed item, the supermarket shelves are extending into the catering sector, in particular fast food. The unit of time is more complicated. The processed item has a consume-by life of around eight days, whereas the fresh pineapple can go much longer, and even too far in terms of the state of freshness of the products on the shelf. Since while the pineapple seems robust, it is because it does not sag like the avocado, banana or pear. It quietly withers, going from a plain green to the most hideous shade of soiled brown, accompanied by a few midges gaily flitting about. Finally, we have already mentioned the radically different positioning in terms of retail price of the two products. Hence the unit of value is completely different. In short, we can easily conclude that there is not much in common between these two segments. The pineapple market will not find its salvation here.

But let’s not spoil our pleasure at seeing the rapid growth of the world market. According to Comtrade, in 2013 it amounted to just over 2.8 million tonnes, i.e. an average annual growth rate over the past twelve years of more than 10 %: a figure worthy of the growth rates of the Chinese economy. It is all the bigger since world production has increased by just 3.6 % per year since 2001. Nowadays, 12 % of world production can be found on the international fresh pineapple market. If we add volumes of processed pineapple (canned and juice) sold, we reach the record figure of 8.4 million tonnes (in fresh fruit equivalent), i.e. doubling the world market in around fifteen years.

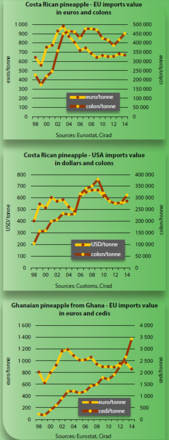

Now let’s turn to the value of the fresh pineapple on the markets. Thierry Paqui, a specialist consultant who edits a weekly letter analysing the European pineapple market, for which you will find further on in the dossier an analysis of the past market season, rates the economic results as highly disappointing. It is not the first time that the downstream segment of the industry has complained of low prices. We have reiterated many times over in these columns the deterioration of fruit market value. Following a purely neo-classical economic rationale, the growth in volumes has caused a fall in value, and even a fall in added value, because of an increase in production costs on top of that. The terms of trade are highly unfavourable for the product. Except that, in theory, the supply should have been adjusted downward. This was the case for the outsider sources which, as we have seen, are deserting the world market. But this free space has been recovered by producers in Costa Rica. The giant has made another step forward. Over the last twelve months (November 2013 to October 2014), Costa Rican exports exceeded 2.1 million tonnes, for an absolute record! But what is the secret of the producers? At the same time last year, FruiTrop (October 2013, no.215) put forward a number of hypotheses. Let’s look at the euro/colon exchange rate. In Europe, the annual average value of Costa Rican pineapples stabilised in 2014 at 615 euros/tonne (estimated figure) as opposed to 617 euros in 2013. Translated into the colon, the observation is very different. Indeed, the revenue in local currency rose 8 % under the spell of the exchange rate. There is a clear and massive impact. This is also the case for fruits exported to the United States, with an even more marked effect, of around 11 %. It is undeniable that the exchange rate is a powerful antidepressant for pineapple producers.

Conversely this advantage, over which producers evidently have no control (macroeconomic data), is not the whole story. Indeed, the counter-example can be found in Ghana. Its fruits were valued disappointingly on the European market in 2014. On average, the fall in euro was more than 10 % from 2013. The situation is turned on its head if we break the exchange rate spell over this figure. The price in cedi actually climbed 29 % in just one year. So long live the devaluation of the cedi! But this wave of the magic wand seems to be having no effect on Ghanaian pineapple exports, which are on a downward trend. It is true that the annual inflation rate amounted to nearly 17 %, thereby reducing the producers’ margins for manoeuvre. By way of comparison, the inflation rate in Costa Rica is far more moderate, around 5 % in 2014, which leaves producers greater latitude.

So the average import prices, after a respite in 2013, have taken a downturn. Spring and summer 2014 were particularly difficult. The average price dropped by half a euro per box to 6.6 euros. Maybe the only minor satisfaction is to observe that the price amplitude was extremely limited both downward and upward. But besides the volumes placed on the market, the supply marking this season was unbalanced with a shortage of small fruits, and therefore an excess of large ones. So much so that at one point, the smallest sizes found takers at prices never reached for this type of fruit: a last straw.

Excessive volumes, for sure, not enough care both upstream and downstream certainly, easing of the fall in import prices via the exchange rate for certain sources undoubtedly, a catastrophe heralded for years which never arrives; in short the fire is smouldering. The coin is balanced on its edge… we just need to see which way it will fall! Is it the time for restructuring and concentrating large volumes in the hands of a few? That is what some are expecting and glimpsing signs of, to finally tell on the natural market trend: the fall in value. But does the only, near-miraculous, solution lie in eliminating the small players? Even if this assertion were valid, the production base in Costa Rica alone is enormous. As we have seen in other industries, small volumes can have big effects. The scattering of production capacities is such that there is a plethora of operators on the market. The local professional association counts more than 170 export companies, and access to long-distance transport is particularly easy. To sum up, operating on this market is like living on a volcano. The earth there is fertile, but you never know what tomorrow will bring.

Pineapple – United States : No limit!

It has been written: US pineapple imports this year will reach 1.1 million tonnes. This is still an estimate, since the customs figures were established provisionally in September 2014. Yet such is the weight of the multi-year trend that there is little risk in extending the curves. If we take away approximately 100 000 tonnes forwarded to Canada, the US market is a millionaire! Costa Rica is leaving just crumbs for its competitors. It holds a 90 % market share, leaving 4 % apiece to Mexico and Honduras. US consumption is slightly different from Europe. Salad bars are one of the major outlets, with demand focused on large sizes (jumbo), and the consumption peaks are slightly different from in Europe. While they are highly marked for the Easter and end-of-year holidays in Europe, consumption in the United States at these times is well below the annual average. Conversely, the months of March, April and May (sometimes June) see the supply skyrocket, up to 50 % above the annual average.

Click "Continue" to continue shopping or "See your basket" to complete the order.