FruitTrop Magazine n°247

March 2017 edition: Mango close-up. The latest on the date market, berries and sea freight.

- Publication date : 4/04/2017

- Price : Free

- Detailled summary

- Articles from this magazine

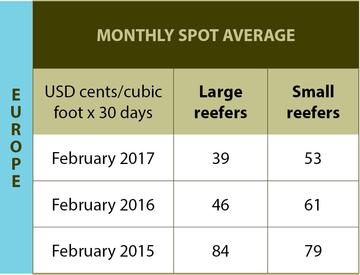

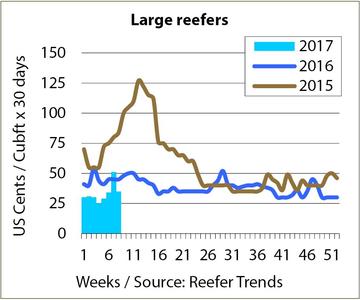

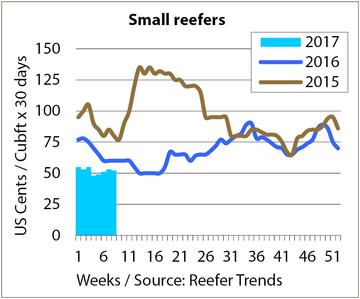

Until or unless the squid come out to play in the South Atlantic in greater volumes, trading conditions on the charter market in February and March are more than likely to disappoint. With only the Turkish port of Mersin able to discharge boatloads of bananas in the Eastern Med, and enough services, slot capacity and equipment for the container lines to build market share on the transatlantic banana strings at any cost, there was no incentive for speculative banana cargoes from Ecuador, not least because of an increase in the exit price as a result of heavy winter rainfall.

Spot activity was restricted to Rastoder fixing a total of 4 small banana cargoes from a limited surplus of Colombian bananas, and a couple of Argentinean topfruit voyages to the USEC and Western Med. Early on, bad weather in the Atlantic also caused disruption, forcing charterers into the market to cover schedules. The marginalization of the specialized reefer on core banana trades puts greater pressure on the mode to deliver seasonal Chilean volumes to the USEC and USWC. The good news for operators is that despite aggressive attempts by the carriers in general, and MSC in particular, to grab market share, the reefer has maintained a strong presence on the two trades.

There may not have been much activity in the charter market in the first two months of the year, but the reefer fleet has been well employed in liner business and COAs. However there is a growing feeling that the aspiration for full employment of the fleet may be as good as it will ever now get, such is the relentless pressure exerted by the carriers. To illustrate the point: the Chilean trade is commercially viable for reefer units with full load factors – but it is unsustainable in the long term unless yields from complementary seasonal southern hemisphere citrus and kiwifruit business are also sufficiently profitable.

The reefer has a chance with bunkers trading at current levels. The issue is however more fundamental: while the mode may be able to compete on cost, it cannot compete on price/rates. And with rates continuing to edge downwards as the lines search for any contribution, no matter how small, to voyage costs, the short term looks bleak. And it doesn’t look much better in the medium term - even once the container industry emerges from its current crisis there is unlikely to be any relaxation in the stranglehold the carriers have on the mode. This is partly because the carriers will not want to relinquish market share back to the reefer, but mostly because the lines will still be competing with each other for hard-won reefer business.

Click "Continue" to continue shopping or "See your basket" to complete the order.

{kind=link}