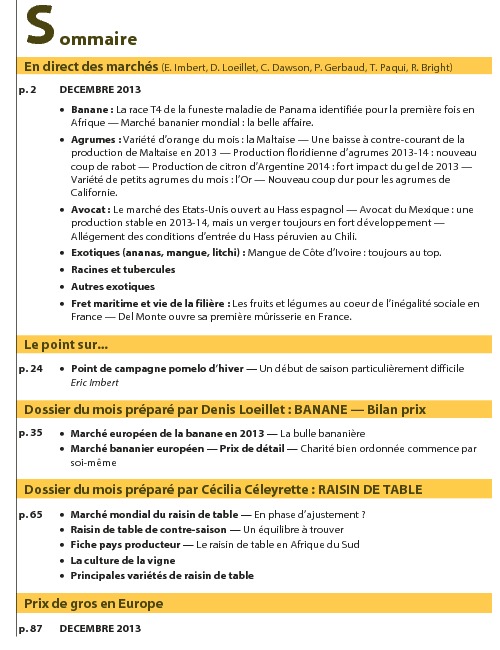

Magazine FruiTrop n°218

Banana close-up

- Date de parution : 29/01/2014

- Tarification : Gratuit

- Sommaire détaillé

- Articles de ce numéro

Five years day for day after the important deregulation of the European banana market, we're still looking for sector players who are still happy about it. Perhaps the virtue of the poor situation in 2010 is, we hope, that it will have given food for thought to supporters of an ever more open European market. Using figures, FruiTrop shows that the changes in this European sector are for the worse rather than for the better.

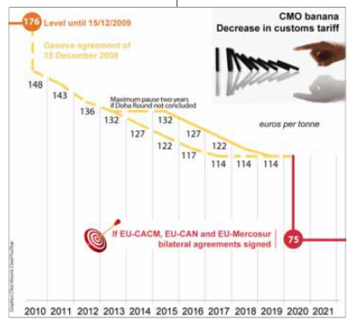

The 17th anniversary of the common market organisation of banana (CMOB) was celebrated on 1 July 2010. However, banana market specialists tend to be more marked by 15 December 2009. That was when the European Union and a few countries dissatisfied with the European banana supply policy decided to more or less finish it off before the WTO. After more than 15 years of legal and political procedures, marathon negotiations and small political arrangements, the CMOB was stripped of all meaning and placed in the already well populated cupboard of agricultural market organisation systems. And many growers, operators and politicians rejoiced at the decrease in the tariff levied on banana imports from third countries (excluding ACP suppliers).

However, the number of rejoicers has decreased strongly a few months after the event. Indeed, the enthusiasm of late 2009 seems to have been quickly dissolved in the worsening of the world banana market in 2010.

Mornings-after can be cruel. Of course, few operators or political officials—especially in Latin America—would agree about a link between the worsening of the market and liberalisation. Their victory took too long to construct and pride prevents people from admitting that their dream has turned into a nightmare. Especially as the disappointment matches the economic stakes.

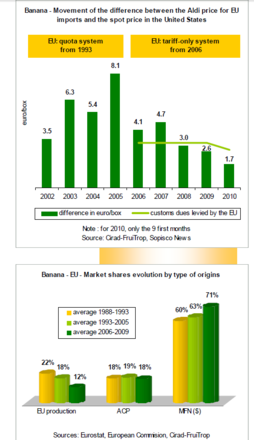

The EU is the world's leading market with consumption of 5 to 5.5 million tonnes and an import turnover exceeding 4 thousand million euros. But above all, it was for nearly 20 years the most profitable market in the world. Before the reform in 2006, the price of a box of bananas was EUR 3.5 to 8.00 more than on the US market. The difference has decreased steadily since 2006 and even reached EUR 1.70 (provisional figure for 2010). This is EUR 1.00 less than the customs tariff (EUR 148 per tonne, that is to say EUR 2.70 per box) levied on EU imports. How the situation has changed! The US market, described as an oligopsony, has become more profitable than the EU.

As regards production, agricultural sectors, chains and even states are strongly dependent on the banana trade with Europe. This applies in particular to the Caribbean states, certain Central American and African countries and most European production zones.

One can thus understand why everybody is interested in the European market. But it is more difficult to understand the advantages of having made it a depressive market. Indeed, the situation in 2009-10 displays, overall, a fall in prices to historically low levels while customs statistics do not reveal any over-supply. And what if this poor situation were in fact a chronic illness caused by the abandoning of market mechanisms that stabilise prices and prevent the destruction of value?

We would thus seem to have reached a system that is in contradiction with the founding principles of the CMOB (Regulation EC 404 / 1993) that were:

Of course, most of these founding principles are no longer topical. But they were only discarded on 15 December 2009. The coinciding of the overall decrease in prices since the end of 2009 at both the import stage (green fruits) and ripened fruits (yellow fruits) and the announcement of the progressive decrease in the customs tariff should not hide the fact that the process of the liberalisation of the European market really started on 1 January 2006. That was the date on which the EU switched from an import quota system to the tariff-only management of imports from third countries. Here, the ACP countries continued to have privileged tariff-free access to the European market but with a quota applied until 1 January 2008.

This reform of the CMOB was performed under the pressure of a few exporting countries in Central and South America, the United States, a few transnational corporations and the approval of a majority of European states. From 2004 onwards, the calculation of the tariff was the subject of intense discussions under the supervision of the WTO (with the price gap calculation principle). The market would no longer be managed by the control of the volumes of bananas from third countries but by the levying of customs dues on arrival of the fruits in Europe. The mechanism is simple: the higher the tariff the smaller the volumes sold because the financial risk becomes too great in comparison with the return that the operator can count on.

What are the effects of this pricing on the main market indicators and stakeholders? The only principle laid down by WTO members at Doha was that total access to the market should be maintained for MFN (dollar) suppliers. In simple terms, the regulatory effect of the tariff should be identical to the effects of a quota system and not be discriminant for bananas from the Latin American zones. Examination of European supply shows that the market is fully compatible with world trade policy. With the exception of a dip in 2009 resulting from a decrease in available supply, the volumes imported have even increased considerably. MFN sources have been successful. From 1993 to 2006, their share of total supply was an average of 63%. From 2006 to 2009 this increased to 71% with peaks at 73% in 2007 and 2008, years in which supply was largest.

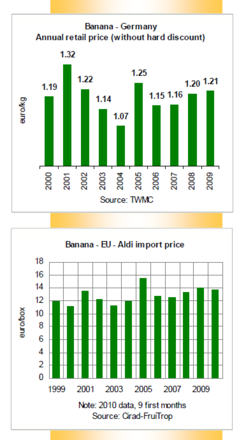

European consumers, often taken as hostages in the negotiations, should be the main winners of the change in regulations and take all the benefit via a drastic reduction in retail prices. Finally, nothing has changed for them. Retail prices in Europe have remained stable or have even risen slightly. In fact, one wonders how they could have decreased! With bottom of the range apples and peak season oranges, bananas are among the cheapest produce in the fruits and vegetables category. At these price levels and given the strong competitiveness in the face of competing fresh produce, one might have doubts about a possible increase in demand if prices were to fall further. We talk in terms of weak elasticity. Bananas are thus a staple on retailers' fruit and vegetable shelves. We could also have said that they are banal as their price and merchant value have little in common with the other produce on retailers' shelves as regards the distance travelled, the work performed throughout the chain and sometimes even the production cost! This year—2010—is also symbolic of the gap forming between falling prices (see below) and an increase of the various intermediate prices: freight charges and fuel, boxes, agricultural inputs, etc.

Summarising this for import prices is not simple. Since 2006, the annual average Aldi price—the reference for imports—has been between EUR 13 and 14 per box. Setting aside unusual years such as 2005, this is slightly higher (not counting inflation) than the level observed during the years preceding the switch to a tariff-only system.

Although import and retail prices have remained stable, consumption has increased. Indeed, supply to EU-27 increased significantly in 2006, 2007 and 2008. The market grew by 600 000 tonnes, that is to say the equivalent of one year of French consumption. Unfortunately, 2009 and doubtless 2010 will display a downward movement of consumption volumes although the total remains greater than 5 million tonnes.

Everything is thus for the best. This is one of the hypotheses. It reassures advocates of an entirely open European market and tells them that they have made the right decision.

It is doubtless not the hypothesis that will be adopted by the producers and states who have complained about returns throughout 2010, on top of the constant increase in intermediate costs. The value of exports is falling, producers' incomes are shrinking rapidly and companies tell their shareholders that times are hard and dividends—if any—will be very small this year.

Another hypothesis might better explain this depressed situation. It is not as nice as it leads to considering that the European and hence the world market has a very fragile balance and certain signs mean that we can fear the worst. The idea is based on the fact that world supply has never been normal since the tariff-only system came into force on 1 January 2006. For several years now, the weather has replaced political and trade regulation. Since 2007, serious damage has been caused by weather in all export production zones (hurricanes in the Caribbean, floods in Central America, tornadoes in Africa, etc.), significantly reducing world export potential. The favourable movement of import prices during this period that has been extremely disturbed in terms of supply confirms that the European market is dependent on world production potential and is directly linked to this. The corollary is that the customs tariff has no effect on the balance of the European market.

Two crises—one in 2006 and the other in 2010—support the hypothesis that the customs tariff has no dissuasive and regulatory effect. We remember 2006 when a Guatemala operator associated with a Southern European counterpart was tempted to come and conquer an Eldorado that was at last open to all without restriction. Spot supplies were delivered throughout the first half of the year, destructuring the European market. The produce did not find takers on the Northern European markets that operate mainly on a contract basis and it did not meet the GLOBALGAP (formerly EUREPGAP) certification conditions required by German retail distributors from January 2006 onwards. In this context, these fruits soon became a low price reference used by all European distributors as a lever to obtain price concessions from traditional operators. After reportedly large financial losses, the European adventure was halted, leaving the market disturbed for many months.

The second crisis is even more worrying. This started in the first half of 2010, one of the most turbulent half-years of the last decade. Continuing under the deplorable conditions of the end of 2009, the European banana market suffered a series of poor performances. Prices were disastrous for the first four months of the year with, for example, the worst January since 2000. The music was the same until mid-May. The average price from January to April was EUR 0.75 per kg, 12% lower than in 2008 and 2009. The return of Costa Rican production and high potential in Colombia contributed to increasing world supply and destabilising all the markets.

Somewhat resigned, operators expected a thoroughly catastrophic year. And this was without allowing for meteorological events which, as usual, changed the situation radically. This time competing fruit sectors were affected: floods in Morocco and Spain at the beginning of the year and then in Poland in the spring, late harvests and production losses, cold, wet weather throughout Europe, etc. In addition, production was short in banana-growing zones as a result of cold weather, volcanic ash, gales, etc. Once again, the weather and not customs dues regulated supply.

However, the improvement in the banana trade was short-lived. The situation worsened again at the end of the summer (mid-September). Prices fell at all stages once again and nobody could tell when the trend would be reversed. The Atlantic hurricane season was active but it did not cause a serious, massive reduction in world supply. Whereas the market had been favourable in general for producers, with Costa Rica and Ecuador even raising their minimum prices several times, this part of the chain is now fragile today. Producer prices are right down. In October 2010, it was reported that Ecuadorean producers were paid some USD 2 per box, less than half the official price. The situation was no better in the ACP zone (in both African and Caribbean countries) or for European producers. Growers in the Canaries regularly leave their fruit unpicked—up to 40% in some weeks—because the market does not pay. European producers are even requesting the renegotiation of the support programme for reasons of the change in market conditions.

These episodes in 2006 and 2010 have revealed two things: extreme market fragility and volatility and the total ineffectiveness of customs dues. Indeed, these have not played the regulation role expected of them. In contrast, they have fulfilled their undertakings as regards the WTO and dollar sources, whose volumes and market shares have increased.

In this situation it is not very clear who has profited from the major upsetting of the European market. The quickest approach is to list those who have not lost out. They are few and far between and in any case lose only rarely. They form of course the final link of the distribution chain. The large supermarket chains naturally prefer plethoric supply and competition between suppliers that increases rather than suffer market regulation that, before 2006, went some way towards re-establishing balance in favour of stakeholders in the upstream part of the sector. Now that the match is over and nothing (quite the opposite in fact) can reverse the downward trend in customs dues, what solutions can halt the forecastable fall in prices? They can be put in three categories:

Very schematically, the EU has two consumer country profiles: the Western European countries, where bananas have been part of dietary habits for many years, and the new member state (NMS) where consumption is about half that of the 'old' European countries. What fantastic potential!

But analysis shows that the calculation is too simple. Account must be taken of the structure of fruit supply in these countries. There are only mass imports if the supply of local fruits is small. If not, consumers go for domestic production, which is also more competitively priced. So the possible gains in volume should be tempered. The situation is clearer in 'old' Europe. Consumption increased on a good foundation in 2007 and 2008 (+ 600 000 tonnes for a constant European area) but the trend reversed in 2009 (- 330 000 tonnes) and the preliminary figures for 2010 do not indicate rapid recovery. In any case, not too much should be expected from banana, the most basic fruit reference, already one of the most commonly consumed and one which only stands out by its low price. Price/demand elasticity is thus very small.

However, the battle has not been lost. The United Kingdom showed the way in the 1990s with the Banana Group project that federated the main market stakeholders for getting on for two decades. UK consumption has increased by 150% during the period whereas it stagnated on most European markets. The programme was finally stopped in early 2005 with economic individuality taking over from the joint objective. Since then, the British market has been the scene of retail price wars that have destroyed value in the banana sector without causing an increase in consumption.

The fruit is accused of many things: banal, basic and characterless. One solution for restoring the attraction and dynamism of the market is the renewing of supply options. Diversification policies are limited for the moment and focused on different production modes: organic and fair trade. But unfortunately the increase in volumes is accompanied by a steady fall in prices at all stages. Prices in the organic and fair trade market segments are converging towards the heart of the market, that is to say traditional Cavendish bananas.

However that may be, other sources of potential growth exist. Purchase and consumption occasions should be multiplied by taking bananas out of the fruit and vegetable department. Thought should also be given to broadening the varietal range, based only on the Cavendish group. There are a great many successful examples of this in other sectors that faced the same problem of falling or stagnant consumption and decrease in value. Club apples like 'Pink Lady' come to mind; these clubs have succeeded in increasing their market shares while containing falling prices at the production stage.

Decreasing market supply is one of the best ways of regaining balance and even of returning a degree of negotiating power to the upstream part of the sector and especially growers. However, in a world in which supply suffers from a structural excess, growers can only pray, get together or make bets.

They can pray that competing zones are hit by bad weather conditions. This is cynical, unfriendly and above all not very effective. Getting together or 'coordination' (a more acceptable term) is no longer topical on a globalised market where each stakeholder designs his own strategy. The Unión de Países Exportadores de Banano (UPEB) founded in 1974 and whose resurrection has been announced regularly dreamed of operating as a cartel by controlling banana supply and demand but soon lost its illusions. All that remains is to make bets on the protective effect of the euro:dollar exchange rate. A strong euro means that the returns in 'dollar' zones automatically increase in local currency. This is the case of Ecuador but not of Colombia or Costa Rica whose currencies are gaining ground against the US dollar. A conclusion seems difficult here as situations vary.

Increasing the value within the sector and sharing it better remains the most sustainable solution but also one whose implementation is the most complex. It concerns the economic and financial interests of each part of the sector. We can only mention and immediately rule out the first way of achieving this: tax banana imports and redistribute the proceeds according to criteria of sustainable development. This idea was put forward by several observers—including CIRAD—in the mid-1990s. It would have made it possible to both regulate the market and guide production towards systems that would be socially and environmentally more sustainable. The world regulatory context now makes it impossible to implement such a proposal.

The creation of surplus value added that would benefit all seems difficult in a context in which diversification policies (organic farming and fair trade) show their limits in terms of value added. In all cases, if there were surplus value this would have to be shared out fairly.

The third pathway is therefore a better distribution of value on a voluntary basis between the various partners in the sector. The FAO has recently set up a working group that is to propose the conditions for such development … unless this is simply THE revolution.

This view of the future is a dark one but it has been seen that solutions exist. As said Romain Rolland, French writer and Nobel Prize winner in 1915, it is necessary to combine 'the pessimism of intelligence and the optimism of determination'. Without this, it can be predicted that the sector will continue to follow a pathway of destructive competition and worsen the terms of trade to the benefit of the links at the downstream end of the chain—to the prejudice of the weakest growers. The sector needs to continue to improve in both an environmental and social manner and nothing will be done without the improvement of the value of produce and fair, balanced distribution of value. The problem is that we are still looking for the collective will to do this.

Denis Loeillet, CIRAD

denis.loeillet@cirad.fr

Cliquez sur "Continuer" pour poursuivre vos achats ou sur "Voir votre panier" pour terminer la commande.

{kind=link}