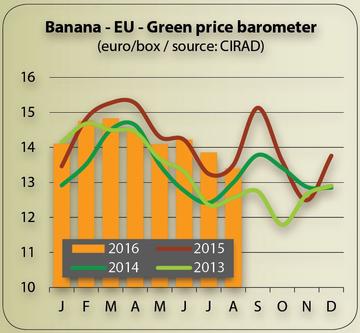

January and February 2016 were marked by lively demand because of the weak competition from seasonal fruits (citrus campaign in shortfall and finished early) and the scarcity of strawberries, including in early spring. As in 2015, the year started with high banana volumes, across all sources, which could have easily been absorbed thanks to the very lively demand. Except in Italy and Poland, prices were higher than the previous year, but also than the three-year average.

We should note a minor turnaround in

March due to a major incoming shipments peak. Volumes from Africa, the French West Indies, Costa Rica and in particular Ecuador more than offset the incipient shortfall from Colombia. Prices dropped to below 2015 levels until

April. Demand was fortunately lively, thereby helping absorb the additional quantities. The Colombian supply, marked by quality problems (effects of the drought), disrupted in particular the East European markets with highly competitive prices. Generally speaking, green banana prices continued their traditional seasonal fall, even dropping slightly below average.

In May, after the Easter holidays, sales saw their usual slowdown, but maintained satisfactory levels thanks to the ongoing cool temperatures and promotions. The dollar banana imports started to fall considerably, with the intensification of the Colombian shortfall, no longer offset by Ecuador. Hence green banana prices held up instead of continuing their traditional seasonal fall. This trend helped prices end up being higher than in 2015 in Poland and Italy.

In June and July, the situation was perfectly managed in terms of procurement, in a favourable context of not excessively high temperatures and a modest stone fruit supply at the beginning of the campaign. Dollar banana volumes were distinctly down from 2015, with the Ecuadorian excess not making up for the wide Colombian shortfall which was at its pinnacle in July. Shipments from Africa and the FWI were moderate until mid-July.

The turning point of the campaign came in

August. Sales were slow at the beginning of the month due to the more marked competition from seasonal fruits and the increasing temperatures. Furthermore, volumes saw a very significant increase across all sources, with in particular the end of the Colombian shortfall and an unprecedented African shipments peak. The adverse impact of the increasing supply and slower demand only started to make itself felt on green prices at the end of month, as stocks were reforming.

banana - EU - green price barometer

banana - EU - green price barometer

{kind=link}