FruitTrop Magazine n°247

March 2017 edition: Mango close-up. The latest on the date market, berries and sea freight.

- Publication date : 4/04/2017

- Price : Free

- Detailled summary

- Articles from this magazine

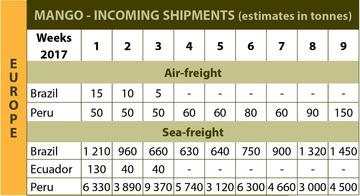

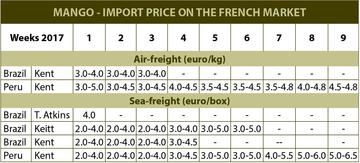

In January, the market sunk into a lasting crisis. The very high tempo of shipments from Peru and declining Brazilian volumes generated large stocks and a drop in prices, which were set on an ad hoc basis in the middle of the month, depending on the merchandise and customers. The dominance of small sizes in the Peruvian supply aggravated the stagnation. This situation extended to all European markets, with equivalent prices all month.

The air-freight market also proved complicated. High quantities and logistical difficulties led to a staccato supply that was hard to manage for the receiving operators, and favoured batches of advanced maturity, i.e. commercially inferior. The end of the Brazilian campaign somewhat relieved the market in the second half of the month, without returning to lucrative prices.

The situation in February carried on from January, with incoming Peruvian shipments still very high. Sales of stocks that had accumulated since the early start by the Peruvian campaign proved very slow. Prices remained at their lowest level, from 2.00 euros/box. The steep reduction in Brazilian shipments had hardly any effect in the first half-month. A recovery phase then began, illustrated by a slight rise in rates, especially for incoming produce. Fruit stocks sold at lower prices. The deterioration in market conditions due to excessive shipments from Peru hastened the end of the Brazilian campaign.

The air-freight market was no more dynamic, with rates often below cost price. In the second half-month, rates recovered slightly because of the change of production zone in Peru. Transport from the landlocked Casma zone to the export airports is more costly. Purchasers baulked at the price increases charged, especially as the produce was more fragile.

Click "Continue" to continue shopping or "See your basket" to complete the order.

{kind=link}