FruitTrop Magazine n°218

Banana Prices Close-up

- Publication date : 30/01/2014

- Price : Free

- Detailled summary

- Articles from this magazine

The European distribution sector played its expected part this year. While the green banana price was slightly down practically right across Europe, retail prices changed for the better. From being a free rider (like Germany in 2012), in 2013 the European distribution sector upgraded to VIP status.

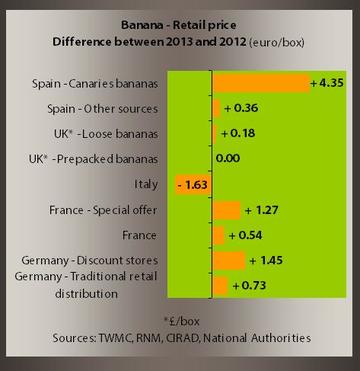

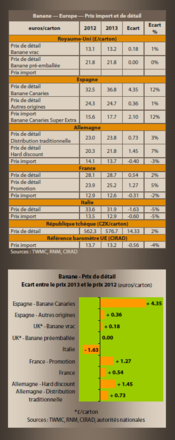

While 2013 was a normal year for the banana in terms of green prices, it was particularly prosperous for the distribution sector. Indeed, as we had pointed out in 2012, the German distribution sector was taking a free ride. It had followed and even greatly intensified the inflationist drive of the green price by fiddling with the labels, readjusting the margins and compensating for (as it was officially put) the continual increase in energy and labour prices. In 2013, we have the same again. German retail prices went up 0.73 euro/box in the traditional distribution sector, and 1.45 euro/box among discount stores. For the latter, this was the same increase as in 2012. In the space of two years, the price per box has gained 3 euros, i.e. rocketing up 15 %. For the banana sector we should not have any concerns about a flat inflation rate, a sign of an economy in difficulty. In this case, it is rather overheating. Although consumers do not reckon on the price per box but per kilo, and a rise from 1.04 to 1.20 euro/kg does not fundamentally change their perception of the product, whereas other fruits (such as the apple) have undergone increases at least as steep. Indeed, the German Statistics Office notes that for the apple the price index went up 15 % in 2013 from 2012, and 20 % from 2011. The trend is the same for citruses, which have rocketed up 15 % since 2011, and 9 % between 2012 and 2013. The fruits and vegetables section is doing better than the food prices index, which slid down 4 % over one year, and 8 % over two years.

In terms of turnover, there is a tidy additional sum for German distributors. With a gain of approximately 900 000 tonnes per year for consumption, and approximately 2.5 euros per box in two years (average between traditional distribution and discount stores), more than 40 million euros have swelled the coffers of the retailers. If the right trend is confirmed on the consumption side, they will have a full house, with a falling (green) purchase price, a rising (retail) sale price and growing volumes. How do you top that?

But we should not be fooled. Unlike in 2012, it is the European supermarket sector as a whole which has taken advantage of the fall in green banana rates to increase its prices. In sometimes excessive proportions, as in Spain, which for its Canaries banana, exceeded the 2 euros/kg annual average mark, i.e. a gain of 4.35 euros/box! In this case the supermarket sector has only passed on, in proportion (+ 12 %), the increase in the green price (benchmark Super Extra). Furthermore, this is the only green price in Europe which has increased. Once again, Spain is bucking the trend for the whole European market, and doing little more than compensating for its awful 2012, which had seen the Canaries green price fall by 17 %.

The French distribution sector also applied an increase. The price per kilo of bananas gained 2 to 5 %, depending on the categories, whereas the green banana price fell by 2 %. The trend is the same for the Czech Republic which increased its consumption prices by 2 %. Conversely, the British and Italian distribution sectors seem to have been aiming for symmetry: when the green price stagnates or falls, the retail price stagnates or falls. Hence for Italy, we might think that competition, exacerbated by the arrival of a big new operator on this market, drove the green banana price a little further downward.

Now let’s analyse more precisely the behaviour of the French market, for which we have a vast battery of indicators. 2013 is not very different from previous years.. There are major principles rooted in the habits and customs of the sector. For example, the retail price is more resilient than the green (import) price or the wholesale price (from the ripening centre). According to our calculations, we can even say that the retail price is twice as stable as the green price. The latter varies on average by +/- 9 to 11 % (2012 and 2013 figures), whereas the retail price only varies by +/- 5 to 6 %. The wholesale price also varies less than the green price, but more than the retail price: by around +/- 6 to 8 %. It is an intermediate commercial and industrial link, which, in some way, dampens the effects of the fluctuations on the world market.

In a highly turbulent period (weeks 41 to 45, see previous article), whereas the green price detached by more than 15 % from the annual average, the retail price fell by 5 to 6 % on average. Another characteristic is the absolute disconnection between retail price and the green and wholesale prices over the summer period. In 2013, we even get a mirror effect. When the green price falls, the retail price rises. Furthermore, although they are concurrent, the two series have no relation between them, since it is the “low season” effect which comes into play for the banana. Big margins are set on products that do not attract regular customers, in the knowledge that if there are sales, the price will not really make a difference.

So now we come to the first part of the year, the first two (rarely three) two-month periods. At this time of year, there is a bigger convergence between the green price and retail price. The latter exceeds its annual average in lower proportions than for the green price. In the first two months of 2013 for example, the green price was 13 % above the annual average, whereas the retail price was just 2 % above its annual average value. This is now a period of very high banana demand from consumers, and the price is a big lever for retailers to attract as many buyers as possible, who of course will not just buy bananas! All of these fundamentals could also be found in 2012, with a few particularities. For example, whereas the green price stagnated at the end of 2012 (5 % below its average), the retail price rocketed by more than 5 %. Finally, the price gaps varied by 0.8 to 1.0 euro/kilo between the retail stage and green stage, by 0.5 to 0.8 euro/kg between the retail stage and wholesale stage, and by 0.2 to 0.4 euro/kg between the wholesale stage and green stage.

Click "Continue" to continue shopping or "See your basket" to complete the order.

{kind=link}