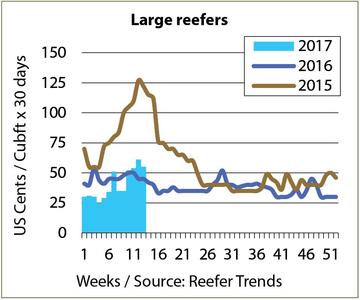

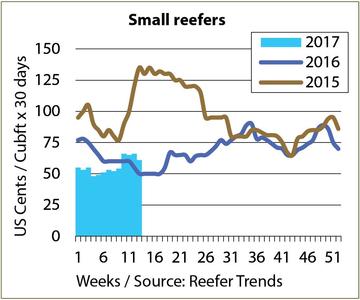

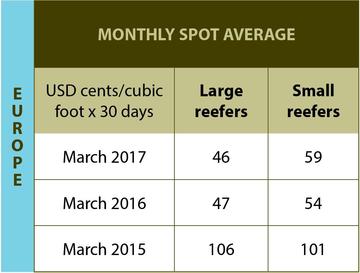

Given the year-on-year increase in bunker prices and no great change or improvement in charter market activity over the period, it should not be a surprise that the TCE average for the first quarter of 2017 calculates lower than the corresponding period in 2016 – for both the large and small segments.

With several vessels redelivering into the reefer pool at the start of the year as the banana majors switched into containers, it could have been worse for operators. However a strong Chilean season absorbed more contract tonnage with higher load factors - as did the squid in the South Atlantic. So while the spot market may have been relatively quiet, the reefer fleet was more optimally employed in Q1 2017 than it was in Q1 2016. And although this development generates more positives than negatives for the mode, the TCE yields on liner business were similarly lower year-on-year. Operators blame aggressive pricing from the carriers for driving down rates and therefore returns.

From now on, things become significantly more difficult. Unless demand for capacity between April and September is greater than it was last year, it is hard to forecast anything other than a long, dry, off-season. This is because while South Africa will export more oranges, the increase will be shipped in containers. Meanwhile, a stronger and longer northern hemisphere lemon season could well see a more modest shipping schedule from counter-seasonal Argentina, and at the last official count, Zespri was planning 20-or-so fewer specialized reefer voyages this season than last – this is exclusively the result of Seatrade re-constituting its New Zealand to Europe Meridian service with its own Colour Class container vessels.

On the positive side of the equation, the Algerian market re-opened to bananas at the end of March. While the quotas and licences favour the reefer mode, this in itself will clearly not be enough to absorb the availability of surplus tonnage over the next six months. It should however go some way towards lifting the burden on Mersin during the September-through-November banana surplus from Colombia and Central America.

sea freight - europe - large reefers

sea freight - europe - large reefers

sea freight - europe - small reefers

sea freight - europe - small reefers

sea freight - europe - monthly spot average

sea freight - europe - monthly spot average

{kind=link}