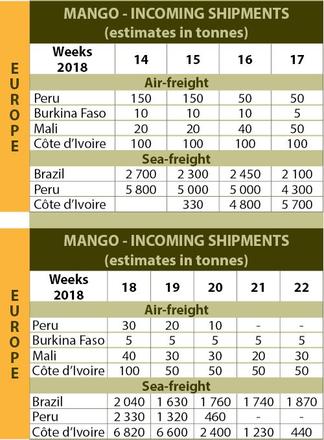

After a slight improvement in March, the European mango market took another downturn in

April. Peruvian volumes held up throughout the month, unlike at the same time in 2017 when they rapidly dipped and caused a supply trough. Meanwhile Brazil increased its shipments, a strategy in place for the past few years to cope with the late start to the West African campaign and the gradual disappearance of Peru. In this context the earlier and quicker start by Côte d’Ivoire led to a substantial and lasting oversupply of the European market. After the Amélie containers received in the first half of April, came a rapid succession of increasing Kent shipments from week 16 onwards. The influx of merchandise of various origins, varieties and quality weighed down heavily on sales, with prices ebbing bit by bit. Far from last year’s record levels, certain transactions were made at less than 4.00 euros/box at the end of the month. In addition, demand was focused more on seasonal products, though scarce and offered at high prices.

The air-freight market fared no better in April, given the ongoing big Peruvian shipments. Many batches exhibiting advanced maturity had to be sold rapidly, which of course led to price concessions. The omnipresence of Peruvian mangos offered at moderate prices complicated mango sales from other origins, especially from West Africa. The often mediocre quality of the Burkinabe fruits (maturation, development) considerably impaired their sales. Kent from Mali and Côte d’Ivoire were marketed, though definitely not at the prices anticipated by the recipients.

May carried on in the same vein as late April, with the European mango market being particularly poor. The extension of the Peruvian campaign with big volumes, plus increasing shipments from Côte d’Ivoire, with on top of that shipments from Brazil and Central American origins, caused a massive oversupply. Consumers switched to seasonal products and the moderate mango demand impaired the sales conditions. Storage also led to a qualitative deterioration of the fruits, consolidating the cycle of poor sales-accumulation of volumes- qualitative deterioration-ongoing low prices. Peru’s withdrawal in mid-May did not provide any improvement, since flows from Côte d’Ivoire and Brazil continued to pour onto the markets. It was only at the very end of the month that sales conditions recovered after a long phase of stock clearances. Côte d’Ivoire was tormented this year between the extension of the Peruvian campaign and concentration of its own tonnages of heterogeneous quality. The rapid dip in availability at the end of the month benefitted produce from Mali and Puerto Rico, which kept better.

The air-freight market too was swollen, with large shipments in excess of the level of demand, increasingly focused on seasonal fruits. The heterogeneity of the fruit maturity made sales difficult and slow. The early start to the Mexican campaign in the middle of the month, although moderate in terms of volume, aggravated the prevailing oversupply. In this context fruits from Burkina Faso and Mali struggled to sell. At the end of the month, the decrease in shipments hinted at an improvement in market conditions for the coming weeks.

mango - europe - incoming shipments

mango - europe - incoming shipments

mango - france - import price

mango - france - import price