Despite the flat market and customary lack of spot activity during July and August, the reefer fleet remained fully employed, inasmuch as all units continued to trade in liner services and/or COAs. The combination of just enough cargo and low bunker prices meant that there was no need for units to lay up. On the supply side, one vessel was reported demolished. On the downside, low rates and idle time left average TCE yields little better than marginally profitable in the best case.

By the end of August it was clear that there were banana volumes surplus to contract requirements east of the Panama Canal. With Colombia expecting to fix 1-2 vessels per week and additional cargo anticipated out of Costa Rica and Guatemala, the market for large units should have tightened significantly by mid-September. If the Philippines also starts calling for tonnage, the charter market will register a stronger performance in H2 than in H1. What happens to banana market pricing in the eastern Med is another matter.

Over the summer the small segment finally started to benefit from the withdrawal of capacity in April and May: operators saw a rise in activity levels and voyage rates as demand from charterers matched the supply of tonnage. However with the Nigerian economy officially in recession, there is an underlying fragility to the market – until the economy shows signs of recovery and the naira strengthens, this is unlikely to change.

The inauguration of the newly expanded Panama Canal at the end of June was supposed to herald a new dawn in container shipping. Well the new era has certainly arrived - it’s just the polar opposite of what had been envisaged! This was supposed to be the age of the ultra-large container carrier, piled high with thousands of steel boxes holding clothing, toys, bananas and Apple iPhone 7s. However it turns out that the world needs smaller, or fewer ships. With so many ULCCs still to be delivered into a global economy that is stuck on super slow steaming mode, the bankruptcy of Korean carrier Hanjin at the end of August may well be the first in a series of container line failures. If so, there will be significant consequences for reefer shipping.

sea freight - EU - large reefers

sea freight - EU - large reefers

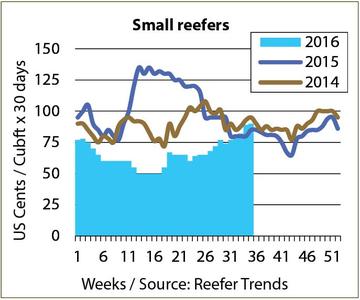

sea freight - EU - small reefers

sea freight - EU - small reefers

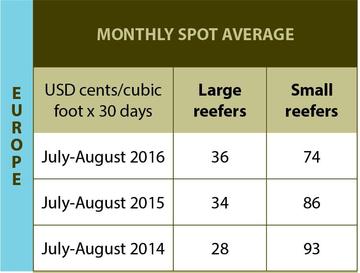

sea freight - EU - monthly spot average

sea freight - EU - monthly spot average

{kind=link}