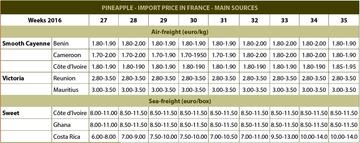

July was marked by a reduction in the overall Sweet supply from Latin America. The volumes received were down by 30 % according to certain operators, because of the end of a natural flowering cycle. As in June, demand was flat, with more interest in seasonal fruits. However, as volumes continued to fall, the rates trend slowly but surely reversed. Still a bit unbalanced by its heavier proportion of small fruits, the Latin American supply sold better and better, despite its fairly heterogeneous quality (affected by rains in Costa Rica).

August brought practically no change to the situation. At the beginning of the month, there was a wide range of rates, with small sizes valued poorly. The flat demand raised fears of a difficult August. Yet this was not the case, since the overall supply, from both Africa and South America, kept on decreasing. From the beginning of the second half-month, the operators learned that the Latin American supply would remain low for several more weeks. Small-sized fruits earned better value, though this did not help offset the shortage of fruits, with certain operators receiving only 10 % of their usual volumes. At the end of the month, the market was desperately vacant. The increase in rates, which went back to the beginning of the second half-month, was steadier, with very high price levels. The end of the holidays and the subsequent re-opening of canteens pointed to rates remaining very high over the following weeks.

In July, the air-freight pineapple market was rather difficult. Despite a fairly limited overall supply, sales followed a false tempo since demand was more interested in the seasonal fruits supply, which was abundant and inexpensive. In addition, we should consider the fairly heterogeneous quality of the fruit from Cameroon, and the fairly poor coloration of the fruit from Benin. Sugarloaf sales (at between 1.80 and 2.00 euros/kg), still very limited, contributed to strengthening the impression of market fragility.

In August, a slight improvement was felt: the supply, just as heterogeneous in terms of quality but more limited, found it less of a struggle to sell. At the end of the month, the presence of some coloured Sugarloaf batches from Benin raised fears of the resumption of MRL checks by the DGCCRF. Making their appearance at the end of the first half of February, Dominican Sweet batches, highly coloured and highly rated, sold throughout the summer on a footing of between 2.30 and 2.50 euros/kg. Note that the week of their arrival, these fruits sold at between 2.70 and 3.20 euros/kg.

July was a complicated month on the Victoria market. Sales were slower since demand was more interested in seasonal fruits. So the operators considerably cut back their imports, to better match demand. In August, demand was no better, indeed quite the opposite. While the supply was even lower (Mauritian supply greatly reduced), sales remained very quiet. Conversely, prices remained stable throughout the summer.

pineapple - france - import price

pineapple - france - import price

{kind=link}